As part of our compliance service for annual accounts and tax, we supply our clients with a bespoke benchmarking report for their practice which analyses their firm’s results for the year whilst comparing this performance against other similar practices.

Clients find the report immensely useful when discussing their annual accounts, and each year we summarise the results in our annual benchmarking review, which covers firms of all sizes across the UK. Where possible, the results are analysed by practice size, which is determined in terms of the number of full equity partners within firms excluding fixed share equity partners and salaried partners. Firms with 1-7 full equity partners are classified small and those with 8 or more full equity partners are classified large. In reality, law firms with more than 8 full equity partners are very much at the larger end of the legal market given the demographics of the sector.

2023/2024 key findings

The key highlights from the 2023/2024 benchmarking review – based on data for the year to date and comprised mostly of firms’ results for March and April 2024 year ends - are as follows:

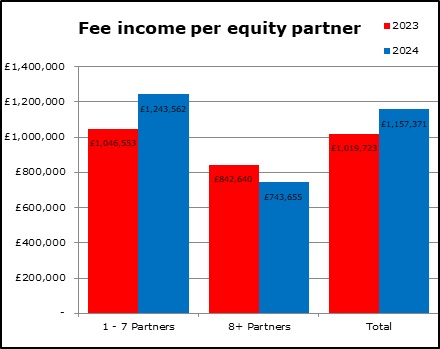

The average fee income per equity partner is £1.18m which is 13% higher than in 2022/23.

The average fee income per fee earner is £159k which is 9% higher than 2022/23.

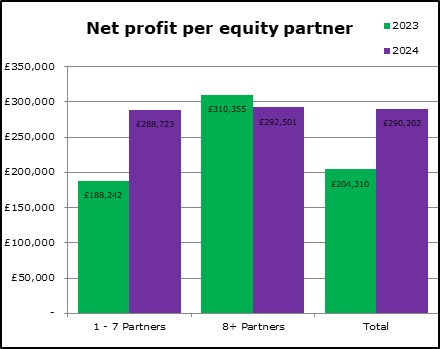

The average profit per equity partner is £290k which represents 32.8% of fee income.

On average there are 7.6 fee earners for every equity partner compared to 6.9 fee earners in 2023/23.

Fee income

Fee income per equity partner has increased substantially by 13% from 2022/23, with average fee income per equity partner now at £1.18m. For a second year, this increase is most notable in small firms where the average fee income per partner is £1,244k compared to £1,047k in 2022/23. Conversely, average fee income per equity partner in large firms has fallen by 12% from £843k in 2022/23 to £744k in 2023/24. This fall is mainly driven by increasing numbers of equity partners in larger firms in comparison to relatively static numbers in smaller firms.

Fee income per fee earner has also increased by 9% upon last year, now averaging £159k.

The increase in fee income for smaller firms is in most cases due to them reviewing and uplifting their charge out rates. Smaller firms appear to have been more adversely impacted by economic pressures – including wages and energy costs - in recent years than larger firms, but they have been reluctant to increase their charge out rates to compensate for such rises. However, this year, we have found that many smaller firms have chosen to increase charge out rates more substantially.

Net profit

Net profit (NP) per equity partner is currently £290k, a significant increase of £86k from 2022/23. Again, as with fee income, this rise is most notable for smaller firms where net profit per equity partner has increased to £289k, up from £188k in 2023/22. This is almost now equal to larger firms where the net profit per partner is £292k. This is a very notable movement, as in the previous year the disparity between the average firm sizes for net profit per equity partner was some £122k.

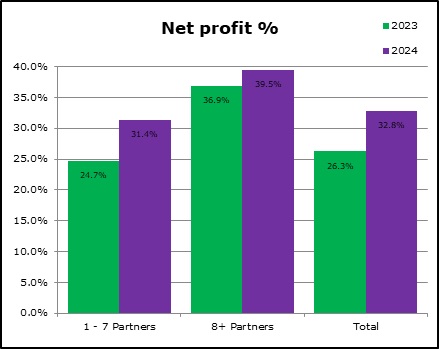

Net profit % has increased from 26.3% in 2022/23 to 32.8% in 2023/24 and firms of all sizes have seen this rise. Again, this increase is most notable in smaller firms, where NP% has increased to 31.4% in 2023/24 from 24.7% in 2022/23.

The overall increase in net profit is down to three main factors:

The recent hike in interest rates has contributed significantly with firms, especially smaller ones, seeing an exponential growth in this temporary income stream. In some cases, interest received has accounted for between 10-15% of net profit for the year.

Smaller firms are becoming better at reviewing their overheads and are trying wherever possible to streamline these.

Many firms are now in a position where they can pick and choose the work they take on, allowing them to concentrate on more profitable work and shifting their split of work types. In some cases, this has been essential to counter the impact of increased lock up caused by court backlogs.

People

On average for 2023/24 there are 7.6 fee earners for every equity partner across all firm sizes.

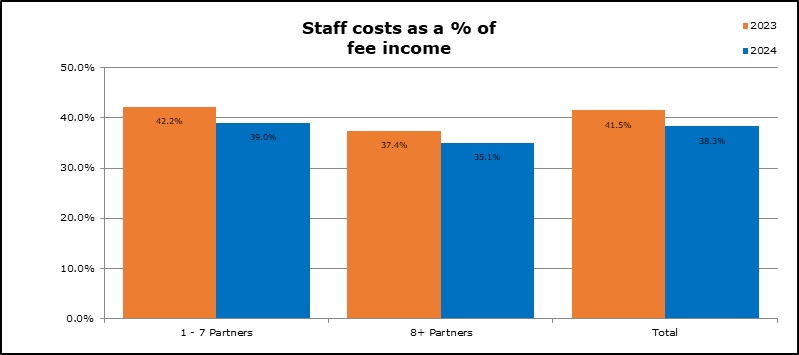

Overall staff costs as a percentage of fee income have fallen from 41.5% in 2022/23 to 38.3% across all firms, with similar decreases in both small and large firms. Percentage costs for smaller firms have fallen from 42.2% in 2022/23 to 39% in 2023/24 and in larger firms from 37.4% to 35.1% for the same periods.

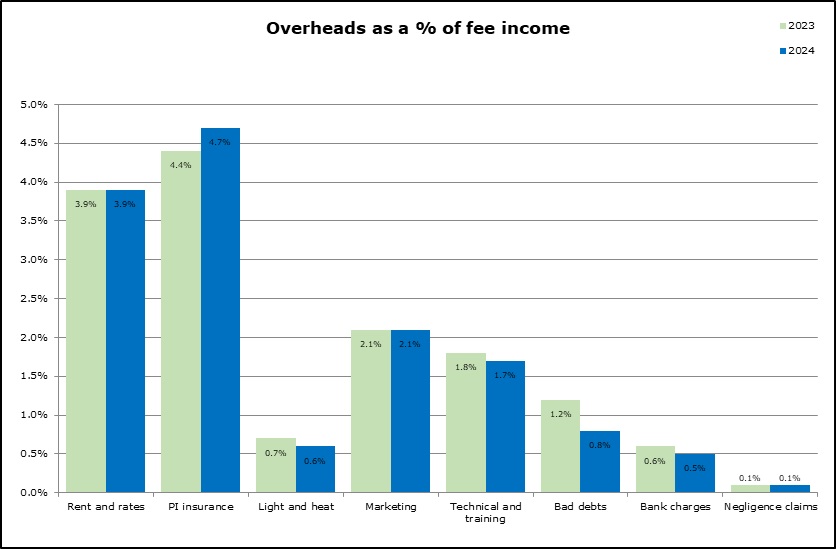

Overheads

Rent and rates as a percentage of fee income have remained unchanged at 3.9%. This suggests that this has now stabilised following the trend for firms to actively reduce office space as a result of offering more home and hybrid working.

PI insurance as a percentage of fee income has seen another rise this year from 4.4% in 2022/23 to 4.7% in 2023/24. As with the previous period, there continues to be a widening disparity between smaller and larger firms. Small firms, on average, have PI costs at 4.9% of fee income compared to larger firms which have a much lower figure for PI at 3.5% of fee income.

Summary

The benchmarking results in our latest review are highly encouraging with both smaller and larger firms showing strong performance, particularly with fee income and interest income. Smaller firms are shown to have notable improvements and are performing on a par with larger firms in some areas. Such smaller firms have been more adversely impacted by wider economic pressures in recent years such as rising staff and PI costs, so it is encouraging to see they are managing to control these factors and produce a strong performance, albeit supported by higher interest rates.

If you are interested in seeing how your firm compares with the benchmarks in this report or want to further investigate variances within your own firm’s performance, then please call 0808 144 5575 or email help@armstrongwatson.co.uk

many smaller firms have chosen to increase charge out rates more substantially.

many smaller firms have chosen to increase charge out rates more substantially.